Last updated: July 17, 2026

If you have a trust, or you're a beneficiary of one, you've probably run into a confusing fork. Some trusts never file their own tax return; their income just shows up on a person's individual Form 1040. Others file a separate return every year and pay their own tax. Same word, "trust," two completely different tax outcomes.

The reason comes down to one distinction: is it a grantor trust or a non-grantor trust? That single question decides who the IRS treats as the taxpayer, and therefore who writes the check. Here's how to tell which kind you're dealing with and who actually owes.

The one question that decides everything

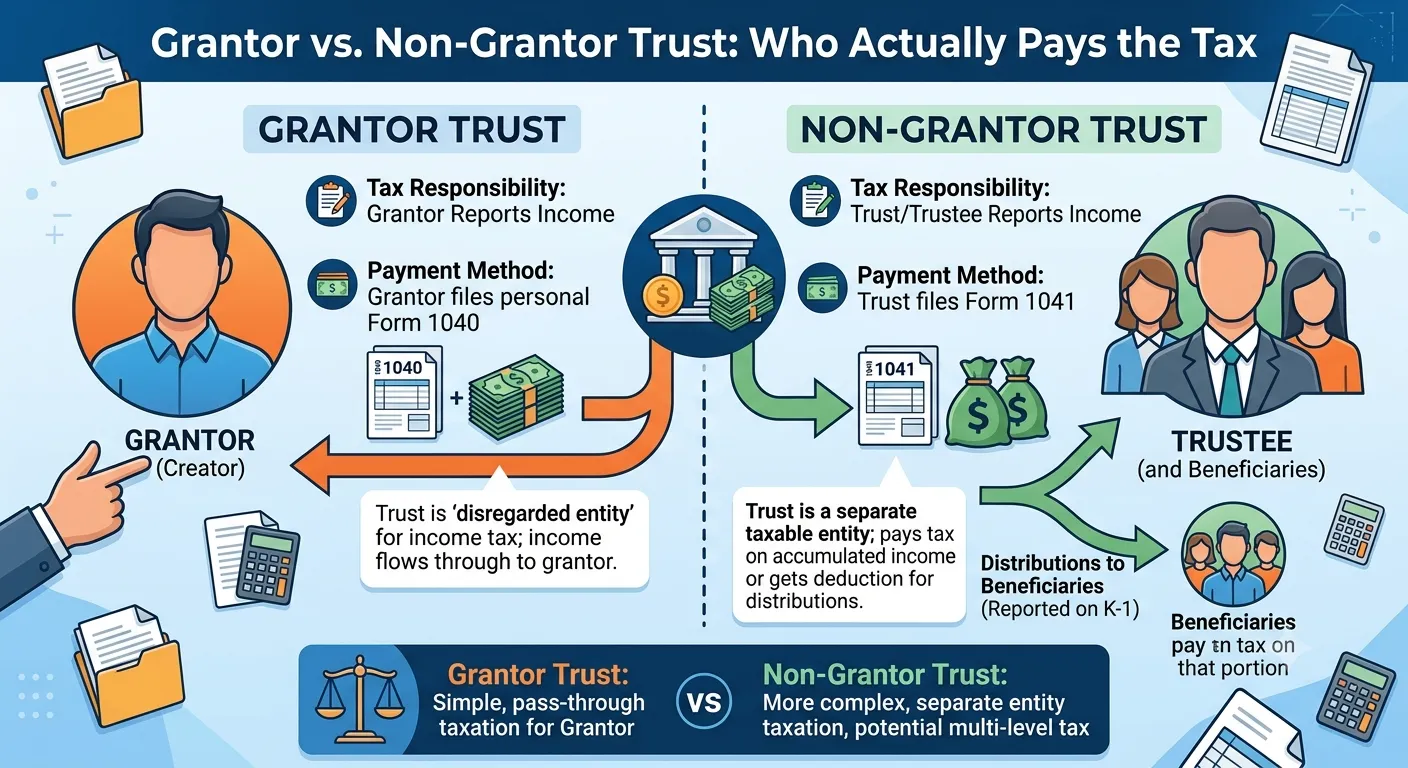

Every trust falls into one of two buckets for income tax purposes. In a grantor trust, the person who created the trust (the grantor) is treated as the owner of its income, so that income is taxed to them personally. In a non-grantor trust, the trust is its own separate taxpayer, with its own tax ID number, that files and pays on its own.

The label comes from a set of rules in the tax code that ask, in effect, how much control or benefit the grantor kept. Keep enough strings attached, like the ability to revoke the trust or take the assets back, and the IRS says you never really gave the income away, so you still owe the tax on it. Cut those strings, and the trust becomes a taxpayer in its own right. Everything else about who pays flows from that.

Grantor trust: you pay, even if you never touch the money

The most common trust in a Texas family's estate plan, the revocable living trust, is a grantor trust. You set it up, you can change or undo it, and you kept full control. So the tax code ignores it for income tax. The interest, dividends, and gains it earns land on your personal 1040 under your own Social Security number, exactly as if the trust weren't there.

The part that surprises people is that grantor trust status can apply even when the trust is irrevocable. Estate planners sometimes design an irrevocable trust on purpose so that the grantor still owes the income tax on it. In that case you can owe tax on income the trust earned even though you have no right to spend a dollar of it. That sounds like a bug, but as we'll see, wealthy families often treat it as a feature.

While a trust is a grantor trust, it usually doesn't pay tax itself. It often files no separate return at all, or files an informational one that simply points the income back to the grantor. The tax bill belongs to the grantor, at the grantor's individual tax rates.

Non-grantor trust: the trust is its own taxpayer

A non-grantor trust is a different animal. The grantor has let go of enough control that the trust stands on its own for tax purposes. It has its own EIN, it files Form 1041 each year it clears the filing threshold, and it pays tax on the income it keeps.

This is where the compressed trust brackets come in, and they sting. A non-grantor trust reaches the top 37% federal rate at just $16,000 of taxable income in 2026, and the 3.8% net investment income tax kicks in around that same level. An individual doesn't hit that top rate until far higher income. So income parked inside a non-grantor trust can be taxed about as heavily as income gets.

A trust generally has to file Form 1041 for any year it has $600 or more of gross income, has any taxable income, or has a beneficiary who is a nonresident alien. Most non-grantor trusts holding real assets clear that easily.

So who actually pays? Follow the income

For a non-grantor trust, the answer to "who pays" isn't fixed. It follows where the income goes.

Income the trust keeps is taxed to the trust, at those brutal compressed rates. But when the trust distributes income to a beneficiary, it generally gets a deduction for what it paid out, and the beneficiary reports that income on their own return instead. The trust hands each beneficiary a Schedule K-1 showing their share, and the tax moves with it. Retained income, the trust pays. Distributed income, the beneficiary pays.

That mechanism is the whole reason non-grantor trusts aren't a tax disaster. If a trust simply hoarded income at 37% while its beneficiaries sat in the 12% or 22% brackets, the family would bleed money to the IRS every year. Distributing income to lower-bracket beneficiaries is how that gets avoided, which is why distribution planning is the heart of non-grantor trust tax work.

Grantor trusts skip all of this. The grantor owes the tax on everything the trust earns, distributed or not, full stop.

Here's the whole comparison at a glance:

| Grantor trust | Non-grantor trust | |

|---|---|---|

| Who the IRS taxes | The grantor (the person who created the trust) | The trust itself, and beneficiaries on income paid out to them |

| Tax return | Reported on the grantor's personal Form 1040; often no separate return | Files its own Form 1041 |

| Whose tax rates apply | The grantor's individual rates | Compressed trust brackets (top 37% at $16,000 in 2026) on income it keeps; the beneficiary's rates on income distributed |

| Taxed on income it keeps? | Grantor owes it, distributed or not | Trust pays on what it retains; beneficiaries pay on what's distributed (via Schedule K-1) |

| Its own EIN? | No; uses the grantor's Social Security number while revocable | Yes |

| Common example | A revocable living trust | An irrevocable trust after the grantor's death |

How to tell which kind you have

You can usually place your trust with a few questions, though the trust document is the final word.

Is it revocable, meaning you can still change or cancel it? Then it's a grantor trust, and its income belongs on your 1040. This covers the vast majority of living trusts. Is it irrevocable? Then it's usually a non-grantor trust that files its own return, with one important exception: some irrevocable trusts are deliberately written to remain grantor trusts for income tax. You can't always tell those apart from the outside, which is where reading the actual trust language matters.

One more trigger catches many families off guard. A revocable grantor trust almost always becomes irrevocable when the person who created it dies. At that moment it typically flips from grantor to non-grantor, gets its own EIN, and starts filing Form 1041. The trust that never filed a return while your parent was alive may owe one the year after they pass.

Why some families want to pay the trust's tax

This is the counterintuitive part. High-net-worth families sometimes structure an irrevocable trust specifically so the grantor keeps paying its income tax, and they consider that a win.

The logic: if the grantor pays the income tax on assets sitting in an irrevocable trust meant for the kids, those assets grow without being nibbled by taxes each year, and the tax the grantor pays further shrinks their own taxable estate. It works like an extra tax-free gift to the trust, one that doesn't count against gift limits. Estate planners call these grantor trusts "intentionally defective," which is a terrible name, because the only thing defective about them is that they're income-tax defective on purpose while doing exactly what the family wants for estate tax. For families anywhere near the federal estate exclusion, $15 million per person in 2026, this is a deliberate and powerful move.

The takeaway isn't that everyone should do this. It's that "grantor trust" isn't automatically bad and "non-grantor" isn't automatically good. Which one serves you depends on your goals and your estate size. The brackets in play often tip the decision.

What Texas does and doesn't change

Texas simplifies one side of this. Because there's no Texas state income tax, the entire grantor-versus-non-grantor question is federal for a Texas trust or grantor. There's no state fiduciary return to file and no state-level trust tax to plan around, which is a real advantage families in high-tax states don't have.

What Texas doesn't change is the federal math. The compressed brackets, the $600 filing threshold, the grantor trust rules, and the distribution mechanics all apply the same way they would anywhere. Texas takes the state layer off the table, but the federal decision about who pays is still where the money is won or lost.

Not sure which kind of trust you're dealing with?

We'll read the trust alongside your estate attorney, settle the grantor versus non-grantor question, and map out exactly who owes the tax before a return is ever filed.

The Bottom Line

Whether a trust reports on someone's personal 1040 or files its own return comes down to a single classification. A grantor trust is taxed to the person who created it, on all of its income, whether or not they ever receive it. A non-grantor trust is its own taxpayer, and its income is taxed either to the trust (on what it keeps, at steep compressed rates) or to the beneficiaries (on what it distributes). Revocable trusts are almost always grantor trusts; irrevocable ones are usually non-grantor, unless they were drafted to stay grantor on purpose.

Getting this classification right, and planning around it, is where real money changes hands, especially for larger estates. If you're not sure which kind of trust you have or whether it's structured the way your goals actually require, that's worth a review with a CPA who handles fiduciary returns and can read the trust alongside your estate attorney.